Canadian Banks Must Power the Platform Economy, Not Just Participate In It

With contributions from Bhavna Wadhwa, CMO of Zafin and Carson Kothyek, Industry Advisor at Zafin.

A Toronto-based small business owner applies for working capital through her accounting software. A Vancouver family pre-qualifies for a mortgage while browsing real estate listings. A Montreal student splits dinner bills through a social app. None of them logged into their bank’s website.

This is the silent shift reshaping Canadian finance. For the first time in modern banking history, the gravitational pull of customer relationships is moving away from financial institutions themselves, not from erosion of the banking model, but from the structural rise of platforms as the new centres of value creation. The centre of gravity is moving from bank-owned channels to platform-owned journeys, where daily financial decisions increasingly occur.

The Fragmentation of Financial Relationships

Financial interactions have morphed into the digital moments that shape our economy. Of the six financial products an average Canadian holds today, roughly half remain with their primary institution. The rest are distributed across fintechs, regional players, and digital platforms. This fragmentation reflects a fundamental change in how loyalty forms and fades.

As younger, digitally native generations such as Millennials and Gen Z, and eventually Gen Alpha, become the majority of banking customers, traditional relationship stickiness will continue to erode.

While 69 percent of Canadians have not changed their primary bank in the past decade, according to FICO’s 2024 Bank Customer Experience Survey, this stability masks generational divergence. Only 89 percent of Canadians aged 18 to 24 maintain a primary account relationship, compared with 98 percent of those over 65, and the gap is likely to widen. For banks, this marks an approaching inflection point. As younger, digitally native generations such as Millennials and Gen Z, and eventually Gen Alpha, become the majority of banking customers, traditional relationship stickiness will continue to erode.

The implication is stark: holding the account no longer guarantees holding the relationship. To remain relevant, banks must move from being product providers to ecosystem orchestrators.

What Ecosystem Banking Means for Canada

Ecosystem banking is how Canadian institutions can leverage their unmatched strengths of trust, scale, and institutional credibility to create and capture value in the platform economy. It means embedding financial capabilities directly into the commerce, lifestyle, and enterprise platforms where Canadians already live and work.

Consider a Canadian homebuyer navigating a real estate platform. They explore neighbourhoods, connect with agents, and receive instant prequalification for financing. Rate comparisons happen in real time. When they make an offer, the mortgage application initiates within the same interface, securely sharing data with the bank’s underwriting systems. Once accepted, insurance, title, and closing services coordinate automatically through the same platform. Post-purchase, the homeowner manages their mortgage, insurance, and home services in one place, without ever logging into a separate banking portal.

This is ecosystem banking in action: the platform drives the experience; the bank delivers the foundation that makes it possible.

The customer never leaves the platform. Yet every financial step that includes planning, financing, insuring, and payment is powered by the bank’s compliance, credit, and scale infrastructure. This is ecosystem banking in action: the platform drives the experience; the bank delivers the foundation that makes it possible. Zafin’s latest ecosystem banking report outlines how this model integrates banks’ regulatory and infrastructure strengths directly into customer journeys.

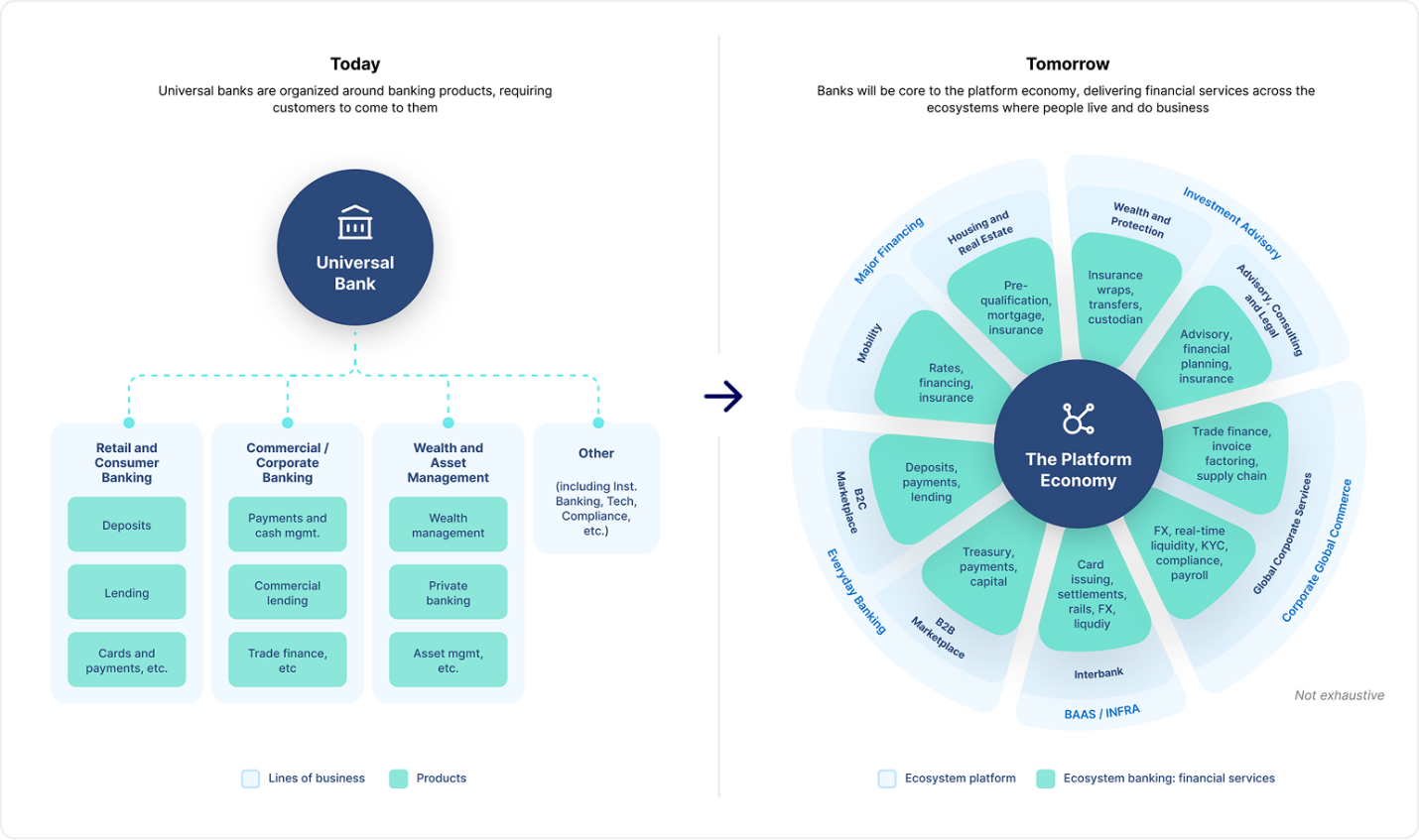

Figure 1: From universal banking to ecosystem banking

Traditional banks have long been organized around internal product lines, requiring customers to come to them. In the platform economy, banks distribute those same capabilities across digital ecosystems, embedding financial services where people live and do business.

Source: Zafin, “Ecosystem Banking: Redefining Relevance in a Platform Economy

Canada’s Competitive Position Amid Economic Uncertainty

Canadian financial institutions begin from a position of strength. Our banks rank among the world’s most trusted, our regulatory frameworks are sound, and the Consumer-Driven Banking Act, passed in June 2024, establishes the legal foundation for open banking. Yet stability can breed complacency.

Shopify, one of Canada’s signature success stories, began as an e-commerce platform. Today, it provides merchants with integrated payments, capital, and business growth tools, functions that once required multiple intermediaries. Interac continues evolving beyond payments into a national infrastructure for digital identity and secure data exchange. These examples demonstrate both what is possible when trust and technology converge and why Canadian institutions must move beyond product ownership to outcome orchestration.

The Endowments That Differentiate

“Trust and scale position Canadian banks as indispensable facilitators of the platform economy.”

What sets Canadian banks apart in the platform economy is two enduring strengths: trust and scale.

Trust ensures safety, compliance, and reliability. Banks hold licenses, governance frameworks, and regulatory relationships that define what is secure and credible in the financial system. They verify identities through KYC standards, secure payments, protect against fraud, and provide a compliance architecture that enables safe commerce, where platforms own the interface, banks supply the assurance that regulators demand, and markets can depend on them.

Scale enables banks to serve as financial infrastructure across markets and ecosystems. When platforms like Stripe Treasury or Shopify Balance offer business banking features, they partner with regulated institutions such as Goldman Sachs and Fifth Third Bank. The platform owns the experience; the bank provides the deposits, payment rails, and compliance stack that power it. In Canada, banks can play the same infrastructure role behind commerce platforms like Shopify and national utilities like Interac, helping to anchor digital ecosystems in trust and regulatory strength.

Together, trust and scale position Canadian banks as indispensable facilitators of the platform economy.

Turning Strengths Into Execution

“Banks must orchestrate complete solutions: financial planning for budgeting, mortgages for financing, insurance for protection, and security for peace of mind. “

Competing effectively in the platform economy requires converting trust and scale into three strategic capabilities:

Customer-obsessed culture. When a customer applies for a mortgage, they are not buying a loan; they are buying a home. Banks must orchestrate complete solutions: financial planning for budgeting, mortgages for financing, insurance for protection, and security for peace of mind. By curating solutions across products and partners into a single relationship, banks transform their scale advantage into customer relevance through seamless, end-to-end experiences.

Value-driven partnerships. No institution delivers every outcome alone. Each must decide which outcomes to own based on franchise strengths, strategic segments, and brand promise. Then they assemble ecosystems of partners to fill capability gaps, extending reach without diluting control. To scale this model, collaboration must be industrialized through standardized commercials, SLAs, consent protocols, liability frameworks, and onboarding processes so partners can connect consistently.

Orchestration and governance. Every customer interaction and partner transaction must be governed automatically, not reviewed afterward. Compliance logic must integrate directly into product configuration, pricing decisions, and partner interactions. The result is assurance that travels with the service, turning governance from constraint into an enabler of innovation.

The Infrastructure Challenge

“Many Canadian institutions continue to rely on legacy core platforms that are often more than a decade old, limiting their ability to deploy new digital solutions and integrate effectively across ecosystems.”

According to Celent’s Dimensions Survey 2025, while 73 percent of retail banks and 81 percent of corporate banks report having ecosystem strategies, only about one-quarter say their current systems can easily support these initiatives. Many Canadian institutions continue to rely on legacy core platforms that are often more than a decade old, limiting their ability to deploy new digital solutions and integrate effectively across ecosystems.

Zafin’s commissioned research shows that real transformation requires two foundational shifts:

- An operating model aligned around customer lifetime value rather than product silos, creating the customer-obsessed, partnership-driven organization needed for the platform economy.

- Platform architecture that operates in three layers: customer experiences and partner platforms at the top, an orchestration layer managing identity, pricing, risk, and compliance in the middle, and core banking systems at the base.

This orchestration layer becomes foundational to the modern bank. It centralizes product and pricing logic, operationalizes compliance at the point of action with explainability and audit trails, and enables shared success metrics that align internal and external value creation. This architecture is what turns offer cycle times from months to days and partner onboarding from projects to plug-ins.

A Call to Action for Canada’s Banks

“By aligning technology and governance early, banks can create the flexibility to adapt seamlessly as new frameworks come into effect. “

Canadian institutions are well positioned to lead the platform economy if they choose to act. The challenge is not whether to modernize, but how quickly leadership teams can align technology, culture, and partnerships around shared outcomes.

- Accelerate regulatory modernization: Work with policymakers to fast-track implementation of secure, consumer-directed data frameworks and digital-identity standards that enable interoperability. By aligning technology and governance early, banks can create the flexibility to adapt seamlessly as new frameworks come into effect.

- Standardize ecosystem governance: Collaborate across the industry to establish common data-sharing models, consent frameworks, and compliance protocols. Standardization will reduce friction, enhance trust, and enable scalable partnerships.

- Invest in orchestration infrastructure: Modernize the systems that manage product, pricing, and partner interactions. Legacy cores cannot deliver the agility or speed the platform economy requires.

- Build ecosystem competencies: Create cross-functional journey teams, partnership-orchestration roles, and shared success metrics that align internal performance with partner value creation.

Path Forward

“The future of banking in Canada is not about where we go to bank. It is about how far our banks can go with us. “

In a slowing economy, margins continue narrowing as platform orchestrators such as commerce marketplaces and super-apps set the terms of engagement set the terms of engagement. Brands fade into the background at the point of decision. Customer acquisition costs rise as regulatory complexity increases. Banks remain systemically valuable while risking commoditization within their own market.

Acting now opens a different path. Trust and scale become levers for growth through partners. Customer outcomes, not products, define value. Revenue becomes more resilient through bundles, dynamic pricing, and embedded distribution. With orchestration and governance built into every layer, banks can move with speed and confidence at scale.

The future of banking in Canada is not about where we go to bank. It is about how far our banks can go with us. The institutions that thrive will combine AI-powered architecture, disciplined governance, and outcome-driven partnerships, anchored in their unique strengths of trust, scale, and institutional resilience. They may not always own the experience, but they will own the foundation of it, serving as trusted infrastructure that powers value across the platform economy.

For Canada’s financial sector, this is not a distant scenario. It is the competitive landscape today. The question is not whether to participate, but whether to lead.

About the Expert

-

Mike Cook is Head of Industry Advisors at Zafin, a global banking software company headquartered in Toronto, Canada. He joined Zafin in this strategic leadership role after a long consulting career focused on banking technology and digital transformation, advocating modernization and customer-centric approaches in financial services.

See more

-

Canada’s Spectrum Policy: Securing Mid-Band Capacity for 5G and 6G Leadership

Canada’s Spectrum Policy: Securing Mid-Band Capacity for 5G and 6G Leadership

Luciana Camargos

Head of Spectrum

GSMA

Luciana Camargos

Head of Spectrum

GSMA

-

Canada Can Lead the World in Open RAN Evolution

Canada Can Lead the World in Open RAN Evolution

Nazim Benhadid

Chief Technology Officer

TELUS

Nazim Benhadid

Chief Technology Officer

TELUS

-

Unleashing Prosperity Through The Power of Procurement

Unleashing Prosperity Through The Power of Procurement

Matt Busbridge

Country Manager

Amazon Business Canada

Matt Busbridge

Country Manager

Amazon Business Canada